Your Guide to UK Tax Allowances

Tax allowances and rates shape how much of your income, savings and investments you keep each year — and they change more often than most people realise.

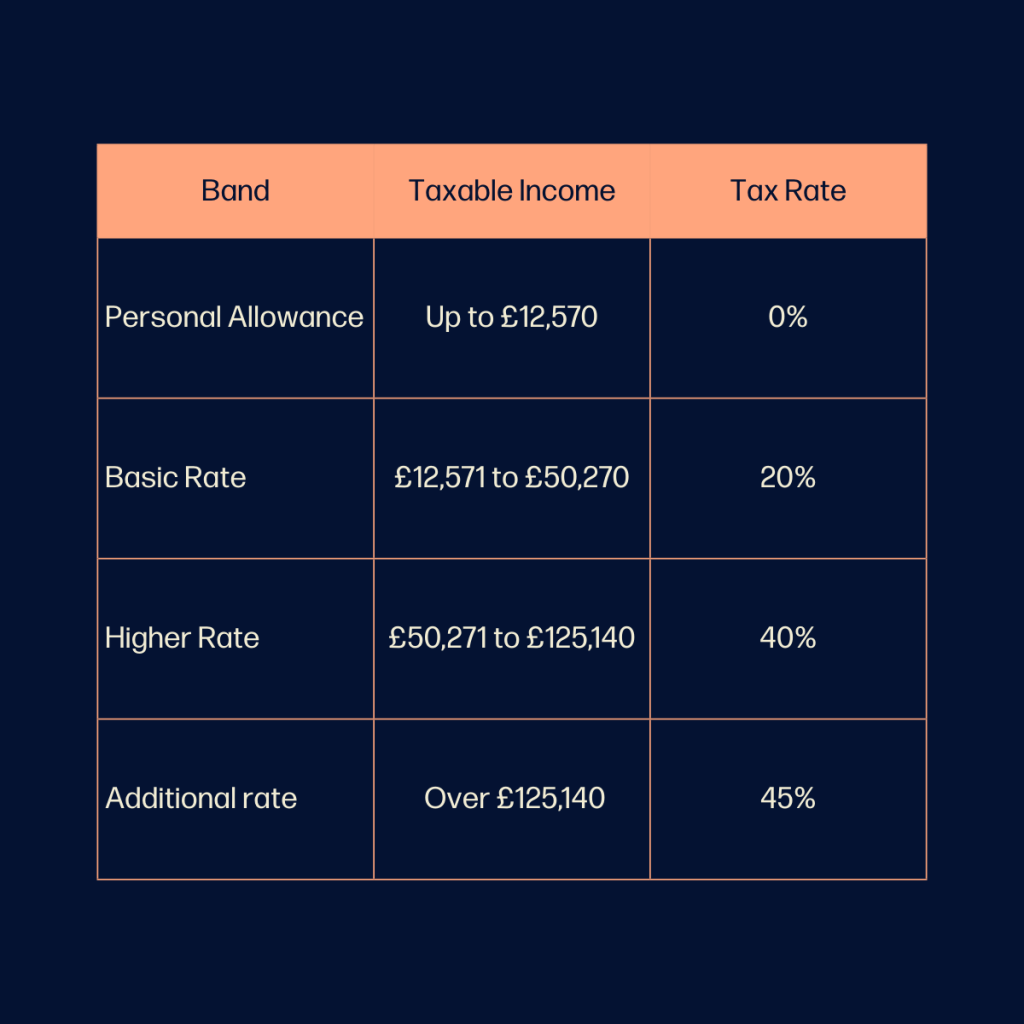

This guide breaks down the key allowances for 2026/27, what they mean for your finances and how you can use them to plan more efficiently.